The riskiest moment for a tuner shop isn't when the car is on the lift — it's after it drives away. The whole purpose of performance work is to push parts and engines past their factory limits, and when something fails at speed, the consequences can be catastrophic: a spun bearing, a thrown rod, a turbo grenading, or worse, a loss of control that ends in a crash. When that happens, the customer — or their lawyer — looks back at the last shop that touched the car. The coverage that defends you in that moment is products and completed-operations liability, and for performance businesses it may be the most important protection you carry.

What "Products & Completed Operations" Actually Means

This coverage responds to bodily injury or property damage caused by:

- Your products — parts you sell or install, whether a turbo kit, a set of rods, a fuel pump, or a software calibration

- Your completed operations — work you finished and handed back to the customer, including builds, installs, and tunes

The key distinction is timing. General liability covers incidents that happen *while* work is in progress or on your premises. Completed operations covers incidents that happen *after* the job is done and the car is back on the road. Without it, you are exposed precisely when most performance failures actually occur — miles and weeks down the line.

The Tuning Exposure Is Unusually High

Most trades have a completed-operations exposure. Few have one as severe as performance tuning, and here's why.

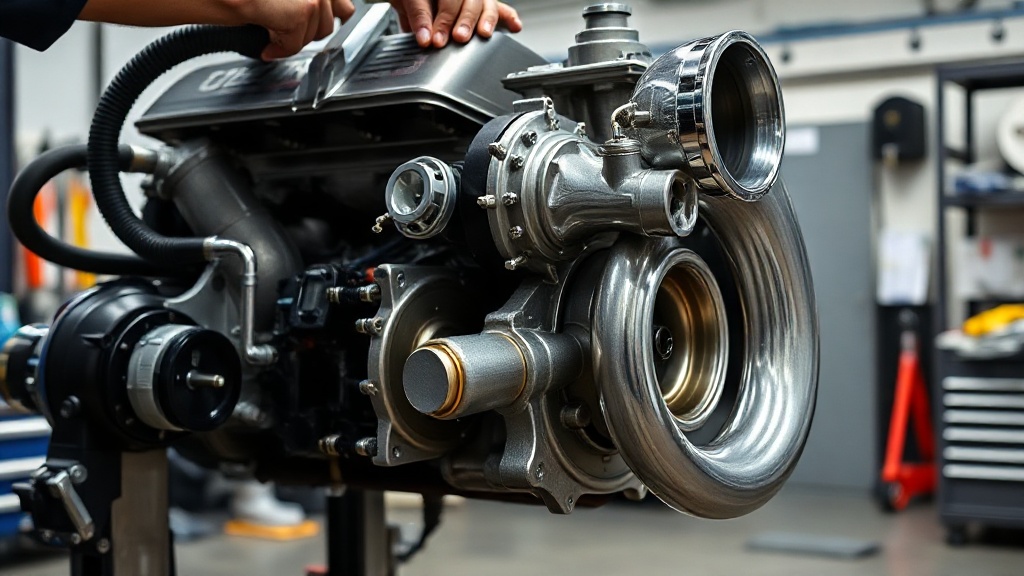

ECU and Dyno Tuning

When you flash an ECU, you are changing fuel, timing, boost, and load targets — the parameters that keep an engine alive under stress. A tune that's too aggressive, that doesn't account for fuel quality, or that masks a mechanical problem can lead directly to engine failure. If a customer's motor lets go and they argue your calibration caused it, you need a defense. Dyno tuning adds the in-shop risk of an engine failing under load, but the bigger exposure is the customer driving away on a map that later contributes to a failure.

Engine and Drivetrain Builds

Build a motor and you've put your name on every fastener torque, every clearance, and every component choice. If a built engine fails and causes a fire or a wreck, completed operations is what responds.

Parts You Sell and Install

Even if you didn't manufacture a part, installing it — or simply selling it across your counter — puts you in the chain of liability. A failed fuel line, a clutch that explodes, a suspension component that breaks can all loop the installing or selling shop into a claim. Products liability covers your exposure for the goods you put into customers' hands.

Why This Coverage Gets Excluded — Check Your Policy

Here is the trap: because this exposure is so significant, some insurers quietly exclude or sub-limit products and completed operations on generic auto-shop policies, especially when "tuning" or "modification" appears in the application. A shop owner can be paying premiums for years and have no idea the most dangerous part of the business isn't covered. Read your declarations and exclusions, and confirm in writing that tuning, modification, and parts sales are included rather than carved out.

Documentation and Disclaimers That Reduce Your Risk

Insurance is the backstop. Good practices are the front line, and they also make claims far more defensible.

- Written disclaimers — make customers acknowledge that modifications void factory warranties, may not be street-legal, and carry inherent risk. Get signatures.

- Off-road/competition-use language where appropriate — document when work is intended for closed-course or off-road use only

- Tune logs and revision history — keep datalogs and a record of every calibration so you can show the tune was safe for the stated conditions

- Fuel and maintenance requirements — record the fuel grade and maintenance the tune assumes, and put it in writing for the customer

- Inspection notes — document the condition of the engine and supporting mods before you tune; note anything that could fail independent of your work

- Build sheets — record every part, spec, and clearance on a build so you can demonstrate it was done correctly

These records don't just protect you in court — they often determine whether a claim is paid quickly or fought for months.

A Real-World Pattern

The typical completed-operations claim follows a familiar arc: a customer leaves happy, drives the car hard over the following weeks, suffers a mechanical failure, and then alleges the shop's tune or install caused it. Whether or not the shop was actually at fault, defending that allegation costs money — attorney fees, expert analysis, and potentially a settlement. Products and completed-operations coverage pays those defense costs and any covered damages, which is why a single excluded policy can be a business-ending mistake.

Protect the Work After It Leaves

Every dyno pull, every flash, every part you bolt on follows the car out the door. Make sure your coverage does too. Confirm that products and completed operations is included at a meaningful limit, pair it with disciplined documentation, and you can keep building power without betting the shop on it.

Tuner Car Insurance, a brand of Contractors Choice Agency, writes policies that keep products and completed operations *in* — not excluded — for performance shops, and we're licensed in all 50 states. Call 844-967-5247 or request a quote through our online form to make sure your most important coverage is actually there.